CCIM Connections

The Official Publication of The CCIM Institute

Image

Image

The Latest Trending Articles

-

Image

Summer 2024

Summer 2024President's Desk

-

Image

-

Image

-

Image

Summer 2024

Summer 2024New Commercial Real Estate Certificate Program

-

Image

-

Image

-

Image

Summer 2024

Summer 2024DEAL MAKERS: Summer 2024

-

Image

Featured Articles by Issue

Stay Up to Date on All Issues

Hero image

Intro Text

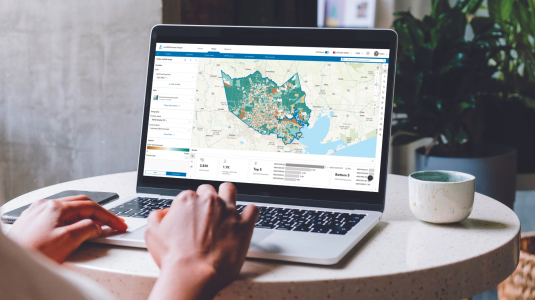

Site To Do Business is commercial real estate's most advanced digital toolkit providing essential data components and marketing tools to give your audience a broader perspective on today's market. By integrating quality online data into a dynamic mapping environment, Site To Do Business provides access to technologies and databases that wins business.

Intro Text

Driving The CCIM Institute's Growth

Hero image

Intro Text

In response to industry needs, The CCIM Institute launches a new program.

Hero image

Intro Text

Making Deals - Spring 2024