Hero image

Image

Understanding Land Value

Intro Text

Residual land analysis is an ideal way to calculate land value based on building area, cost estimates, and development risk.

Body

By Michael J. Rohm, CCIM, MAI | Summer 2022

Residual land analysis is a method for determining the value of development land and is calculated by subtracting all costs associated with development from the total value of a hypothetically complete development, including profit but excluding the cost of the land. The amount left over is the residual land value — or the amount the developer can pay for the land given the assumed value of the “as complete” development, the assumed project costs, and the developer's desired profit.

In its simplest form, residual land valuation follows this formula:

“As Complete” Value

- Cost of Development

Land Value

In other words, the land residual analysis answers the question: “What can I pay for land in order to maintain project feasibility?”

Although our attention is primarily on commercial real estate, the most understandable application of the land residual formula is with residential lots in a tract subdivision, because of the relatively small variations in the completed home values. This consistency translates into more credible “as complete” value estimates. The residual land valuation will always begin with the “as complete” value of a proposed development alternative. For instance, in the case of a tract development, a custom homebuilder will offer a buyer seemingly endless upgrades. Not all upgrades will be financially feasible. Some will be, but most will not, as the upgrades — and more importantly the combination of the upgrades — will not perfectly reflect typical market desires. These upgrades often reflect personal tastes and wants, which are rarely consistent with the typical market participant and may not always optimize the property's resale value.

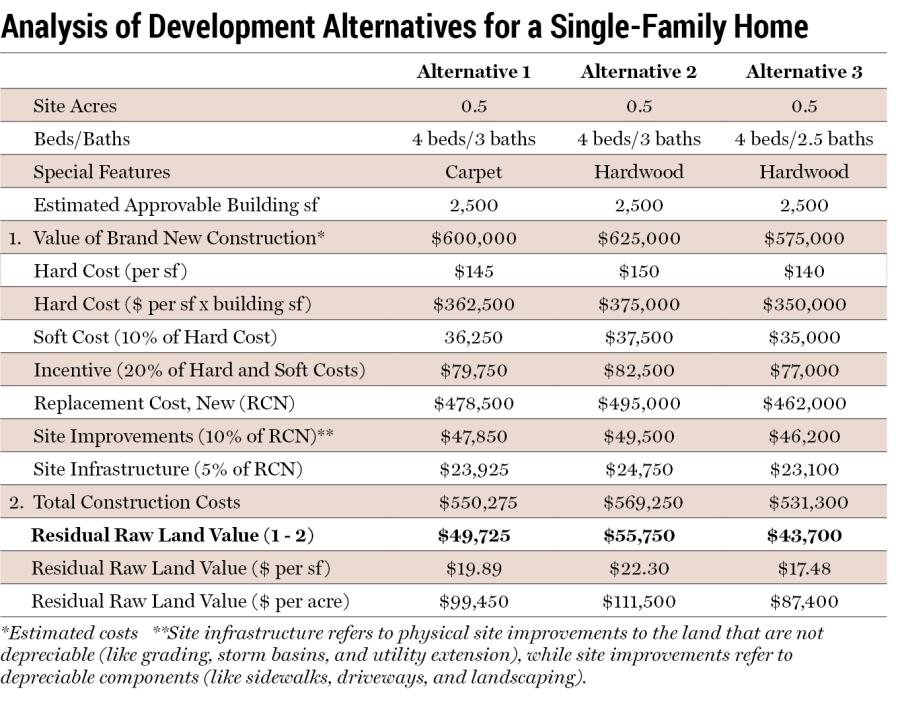

Upgrades and alternatives for custom homes are not always limited to interior modifications; they can include differences in size and exterior building materials. For our discussion, we will focus on interior alternatives to show the concept of a residual land analysis. The table (on pg. 15) shows a land residual analysis based on three development alternatives.

Image

Alternative 1: This option is a 2,500-sf single-family home with four bedrooms and three bathrooms with carpet throughout (with the exception of the kitchen and bathrooms). This home costs $550,275 to develop and will be worth $600,000 when complete. The analysis translates into a residual land value of $49,725 ($600,000 - $550,275) for an approvable raw lot.

Alternative 2: This option is the same as Alternative 1, only with hardwood floors throughout (except for the kitchen and bathrooms). This home costs $569,250 to develop and will be worth $625,000 when complete. The analysis translates into a residual land value of $55,750 ($625,000 - $569,250) for an approvable raw lot.

Alternative 3: This option is a 2,500-sf single-family home with four bedrooms and 2.5 bathrooms with hardwood floors throughout (except for the kitchen and bathrooms). This home costs $531,300 to develop and will be worth $575,000 when complete. The analysis translates into a residual land value of $43,700 ($575,000 - $531,300) for an approvable raw lot.

As is inferred via the analysis, hardwood floors cost more than carpet and bathrooms cost more than common areas. Bathrooms and hardwood floors also contribute more value to the property, all else being equal.

Based on the residual land analysis, a four-bedroom, three-bathroom home with hardwood floors throughout (Alternative 2) is the highest and best use for the vacant site because it produces the highest residual land value. Put another way, this is the development alternative that returns the most value to the land.

One weakness in the land residual approach is the sensitivity of the analysis. This approach is limited as the value and costs are dynamic, which will be reflected over the course of the development rather than at a single point. For example, rising labor and material costs along with unforeseen expenses associated with site infrastructure could increase the final development costs, which in turn negatively impact the residual land value. This approach to analysis also does not explicitly consider holding costs and time value of money, so it is important to consider recent land sales to support the conclusion.

The weakness in relying exclusively on comparable land sales is that buyers do not always make land purchase decisions based on the real estate-related financial feasibility of proposed improvements — especially proposed build-to-suit improvements for owner-occupants or partial owner-occupants. From a commercial development perspective, owner-user decisions are often based on enhancements to business/brand value as a result of relocating, renovating, or ground-up developing in a visible or accessible location. These development decisions rarely result in real estate financial feasibility due to the location and development criteria being specific to each user. In other words, the project may be financially feasible, holistically, but it is not financially feasible from the real estate value perspective alone. This is a concept known as “transferred value,” which contends that a development may be financially feasible if one considers the enhancement to business/brand value as well (i.e. not all of the project value is derived from real estate). In this way, owner-users who develop land may employ a land residual analysis based on a combination of 1) the value of the real estate when complete, and 2) the increase in business value from having a better location and newer buildings to attract clients, thus resulting in a willingness to pay an amount for land that rarely pencils when viewed strictly from a real estate financial feasibility perspective.

Another weakness in utilizing the land sales comparison approach exclusively is that without a site survey or engineer analysis of development potential based on zoning and setback requirements, the differences in development density between sites may significantly deviate, making any comparison less credible. In short, the residual analysis is an ideal analysis if the approvable building area, estimated cost to construct, and development risk are credibly input.